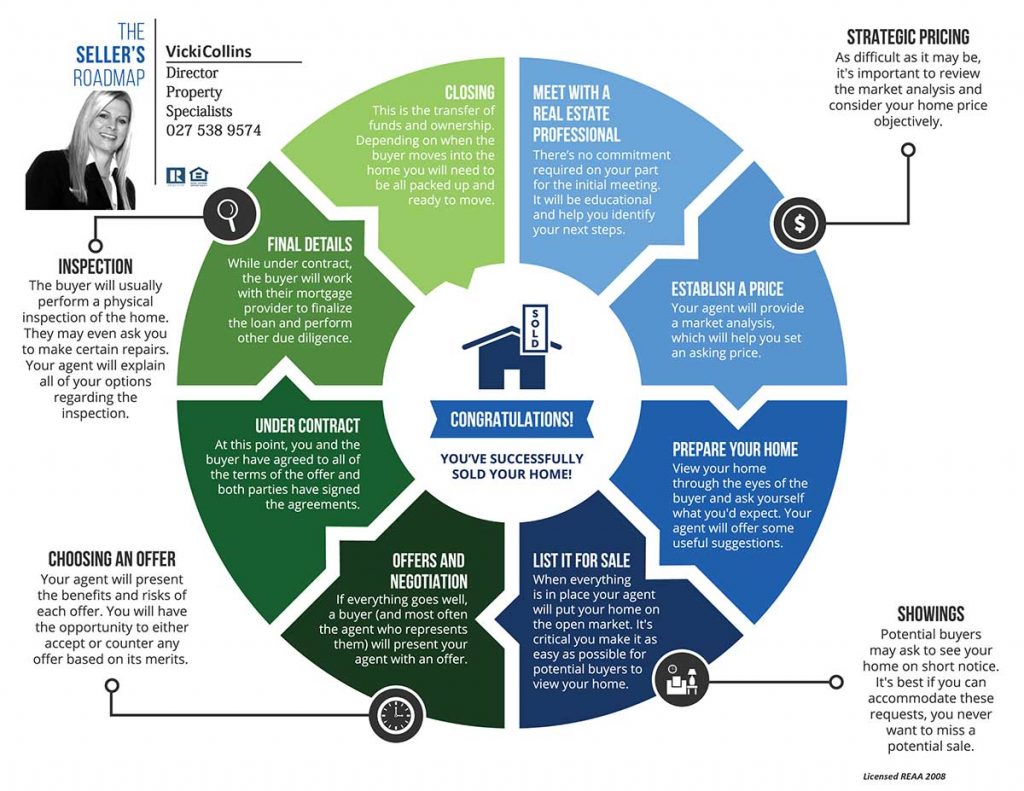

Selling your home is a complex legal process. Whether it’s your first home, or you are an experienced seller, it’s very easy to forget things and to feel overwhelmed.

All properties will sell in a range that is determined by location and condition of your property, comparison with similar properties in the area and the ability of the agent you select to handle and negotiate the sale process

- Sign up with a real estate salesperson

- Your real estate salesperson works on your behalf, so it’s important to choose someone you feel comfortable with.

- Discuss everything carefully with your salesperson before signing an agency agreement with your salesperson will do all of the following things:

- Give you a written estimate of your sale price. This must reflect market conditions and be supported by information about sales of similar properties.

- Discuss the different options for selling your property. You can choose to sell at an advertised price, or by tender, auction, or deadline sale. Your salesperson must tell you how the option you choose affects the commission you’ll pay them.

- Give you a written estimate of the commission. They must tell you how they’ll calculate the commission and when you must pay it by.

- Give you a copy of the New Zealand Residential Property Agency Agreement Guide. They’ll also ask you to confirm in writing that you’ve received it.

- Explain how they’ll market your property and how much the marketing will cost. Some marketing may be free, but you may want to pay for additional advertising. (You usually have to pay upfront).

- Explain the risk of paying two commissions. This is a risk if you enter into more than one agency agreement.

- Give you the opportunity to seek legal advice before signing an agreement. You should take this opportunity. Making sure everything’s in order at this stage could save you problems later.

TIP: Remember that the salesperson works for you. They must always treat you fairly and represent your best interests.

2. Understand the sale process and method of sale

- There are several methods of buying and selling property – for example, tender or auction. It’s important to understand the process you’re using to sell your property. Practices can vary between agencies, so make sure you confirm details with them.

- Your salesperson will prepare a marketing campaign, advertising material, script for the internet

- Sign off on the above

- Have professional photos taken

- For Sale sign erected

- Salesperson will conduct buyer inspections, open homes and team viewing

- Salesperson will contact data base to let them know your property is on the market

- Flyers delivered in your area to also let the neighbourhood know that your property is for sale

3. Read the sale and purchase agreement

The sale and purchase agreement is legally binding, so it’s important to read it carefully and get legal advice before you sign. You can negotiate the terms and conditions of an agreement, but once you sign it, there’s no going back.

The salesperson must give you a copy of the guide before you sign a sale and purchase agreement. We recommend reading the guide early in the selling process.

Know what’s in the sale and purchase agreement

The sale and purchase agreement sets out all the agreed terms and conditions.

Basic clauses

These include:

- the price

- chattels (for example, fixed floor coverings, whiteware or curtains) included in the sale

- the type of title (for example, freehold or leasehold)

- any conditions you or the buyer want fulfilled before you agree the contract

- the date the agreement will become unconditional

- the settlement date

- any deposit the buyer must pay.

Clauses about obligations and conditions

The agreement also includes clauses that set out obligations and conditions that you or the buyer (or both) must abide by. These may include what access the buyer can have to inspect the property before settlement and ensuring the property remains insured until the settlement date.

Clauses about default by you or the buyer

Clauses are also likely to cover what happens if you or the buyer default. This covers compensation that you or the buyer must pay if either defaults on the terms of the agreement – for example, by delaying settlement. Your lawyer can explain these clauses to you.

Understand that you can’t change your mind after you’ve signed

In general, when you’ve signed the agreement and the conditions set out in the agreement have been met, you have to go ahead with selling your property.

TIP: Remember, you can negotiate the terms and conditions of an agreement, but once you sign it, there’s no going back.

4. Understand the language of property sales

The property market has a lot of words and jargon that may be new to you. Use our handy glossary to find out what everything means.

5. Find out more about REAA

There is a an independent government agency. We’re here to help and protect people buying and selling property. Visit our website for more help and advice. www.reaa.govt.nz

6. Get legal advice

You want to get a good price for your property, and you need to know your legal obligations when selling. That’s why it’s important to get your own legal advice before you sign anything.